Spanish Nano-Cap, poised to grow double digits EBITDA and trading at a 7x EV/EBITDA - Tier1 Technologies S.A.

Tier1 Technologies

Disclaimer: This article is for informational and educational purposes only. Do not interpret anything below as financial advice. Always do your research & speak to a financial professional before making investment decisions. Stock prices and market value have changed since the time of writing. This is NOT a buy or sell recommendation.

Additionally, do consider that this is my second largest position, which introduces biases.

Firstly, I want to thank Sven (Twitter: @FinSkeptic, Substack: ) for introducing me to this idea, sharing some of his research with me and for all the help.

Introduction

A Software and IT-Services business focusing mostly on the retail sector in Spain

c.50% of revenues and all the EBITDA can be attributed to the Software Segment, whilst 50% of revenues and 0% of EBITDA can be attributed to the IT-Services segment (based on H1FY23 numbers)

c.50% of revenues are recurring, through LT maintenance and license contracts

Summary of the Thesis:

Extremely high upside if everything goes right, quite high upside on a base case scenario and a limited downside due to low valuation and insider ownership

Management owns 57% of all shares (c.45% CEO)

IPO in FY18

Marketcap.: 24MEUR, EV: c.21MEUR

Multiples (Share Price used: 2,4EUR)

7x EV/EBITDA(FY23)

Somethings to consider:

This is an extremely illiquid stock, with most of its filings in Spanish

Float: c.43%, if we excl. 2 large institutional investors its c. 30%, or a float of c.8MEUR.

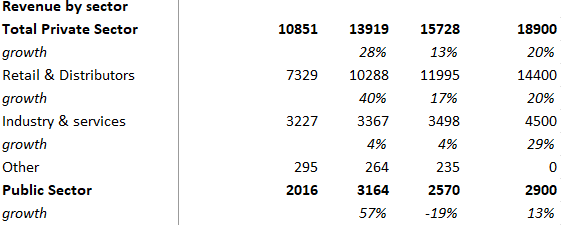

Segments

Software

Around half of the revenues are recurring, through licenses

Order intake up c.50% FY22 vs FY23

Revenue Distribution:

2/3 Comerzzia and 1/3 other

Comerzzia

Comerzzia is a inhouse developed omnichannel retail software solution and platform, which is one of the most comprehensive omnichannel solutions on the market and the key driver of the investment thesis

Sales via recurring license agreements

Included solutions: scan and go, ERP system, inventory management, e-commerce (great to have an e-commerce and Inventory management in one solution) and many more

Many competitors don’t have all these solutions in one, which is a key selling point for Comerzzia

Gartner, has recognised Comerzzia in several editions in its guide: “Market Guide for POS” as one of the most relevant platforms worldwide for the management of store chains

Gartner is a very important IT research company, all the large IT-services reference them as one of their key sources

Value proposition:

Comerzzia shares its source code with partners and clients, guaranteeing total autonomy to customise the solution and easy & fast implementation.

Increased revenue

Full control of data (the customer and his behavior)

Scalability (verticals, market and omnichannel)

Support (implementation, operation and evolution)

Guarantees and trust (Gartner, customer and partner reference).

True Omnichannel Solution, has everything one can think of

Current focus:

International Expansion

Adding more capabilities

Other Solutions

Elevatorware

Software for elevators

Securinvoice

E-invoicing solution, transmits info from clients to tax-software solutions

In the future every firm in Spain has to send all bills to the state, so these types of solutions will be high demand

The management sees large potential here

My estimate 1-5MEUR revenues in the next few years, with high margins due to no implementation costs (sends info from A to B, in a structured way. Not like Comerzzia where large implementation is needed)

Lustrum

Software for Maintenance and cash control system

(A ticketing solution)

Engage

Supply Chain Management software

Atractor ERP

Typical ERP system

IT-Infrastructure / IT-Services

Construction, evolution, implementation and maintenance of software, Deployment and maintenance of IT infrastructure...

Typical IT-Services company focused on software and hardware

Quite Bad margins: 0-5% (normalized)

Due to the high degree of Trade

In the long term this will probably change due to them focusing more on higher quality contracts

Thesis

I’ve split my Thesis into: (1) Drivers sorted by estimated time of impact on the stock price and underlying business (2) Drivers sorted by source of value creation

(1)

1. Short-Term (1 year)

Operating leverage, is starting to show. Driven by their Software products, mainly by Comerzzia. This seems to have been overlooked by the market

Information inefficiency

A presentation for the FY23 numbers was already released, but didn’t get much attention, it included very positive EBITDA, revenue and segment data. Once this info hits the information providers this name will probably pop up on many screens.

I assume this will happen once the Annual Report is published(probably in late march)

It might include a new strategic plan with clearer goals (as in revenue & earnings est. for the long term), giving us better visibility

2. Medium-Term (1-5 years)

I believe that:

Comerzzia is going to continue to grow strongly, with high operating leverage

Other Software might also contribute strongly in the medium term (such as Secureinvoice)

IT-Services will see an increase in EBITDA by focusing more on maintenance contracts instead of trade revenues

International Expansion will be one of the key growth drivers for software and might lead to explosive growth

3. Long-Term (+5 years)

Comerzzia M&A

A successful continuation of the current M&A spree of low valuation, small and value adding companies, might create an immense amount of value in the long term

I believe that Tier1 might copy the Comerzzia strategy in other areas

Creating new platforms, in which they can plug in cheaply acquired companies and creating synergies

(2)

IT-Services

They should grow top-line, 5-10% and are improving margins by focusing on maintenance contracts instead of trade

Top-line growth is driven by implementing Software products, as well as the general digitalisation trends

Comerzzia:

A strong retailing platform with multiple strong partnerships, ready for international expansion, with highly recurring business and high switching costs

Growth drivers

M&A: Acquiring businesses and adding their services / add-on solutions to the platform

Organic: growth in demand for digitalization of retailers

International sales: through a Joint Venture (Brazil), fully owned companies (US or Portugal) or partnerships (Retex)

International Expansion

1. Smaller Opportunities

A 100% Comerzzia owned subsidiary with unmeaningful revenues up until now in the US

It was incorporated in 2019, but over the past year, they've been increasingly talking about expanding into the US. So, there could be a shift in focus in the medium-term.

CPI retail, a company they acquired in FY21, operating in Portugal

This added Portugal to the sales network of Comerzzia

50/50 owned JV in Brazil (since FY22)

2. A Large Opportunity in Italy - Retex

Retex is a retail consultancy focused on IT and Marketing in Italy with many very large clients (Starbucks, Lavazza, Carrefour...)

100M revenues in FY22 and strongly growing

They have been shifting their focus towards implementing omnichannel solutions

They are a new Comerzzia gold partner, and had to have indulged in a lengthy process of training employees

This heavy investment is a clear indicator that Retex wants to sell Comerzzia solutions soon

I assume we will start seeing effects of this partnership in FY24

Management

The CEO of Tier1 and the Manager of the Retex food and retail segment talked very bullish about the partnership

Risks

CEO

He is quite new to the capital market, IPO in FY18, and said in a recent earnings call he wants to possibly dilute shares too acquire an anchor investor.

This might also have been a translation issue

In a Call, which a friend of mine conducted with the head of M&A of Tier1, she said that this is no longer a focus and wont happen

Safety against too high dilution or other shareholder unfriendly behaviour is the Managements ownership of shares (c.57% of total shares)

Lower growth

Comerzzia might only grow topline high single digits and partnerships might not bring the anticipated revenue rise

At high single digits topline growth, this opportunity still seems great due to the operating leverage on the software side

Bad Capital Allocation & M&A

Very short track record

Currently the M&As seem very consistent with the strategy and prices paid are very low

Also c.50% of net income is paid out as a dividend, clearly showing that the Management is interested in giving back cash to shareholders

The aforementioned reasons, as well as their consistent communication over years, gives me a high degree of confidence in management's capabilities to allocate capital in the shareholders best interest.

Growth strategy (As of FY23 Presentation)

Objectives:

1. INTERNATIONAL DEVELOPMENT

Press Release 19.5.2023 – “celebrating 30 years since founding”

They highlighted “the growth in international clients with Comerzzia in Portugal, Italy, the US and LATAM.” in this press release

2. LEADERSHIP IN THE RETAIL SECTOR

3. "RE-ENGAGEMENT" OF THE INDUSTRIAL SECTOR

4. GROWTH AND PROFITABILITY

How:

1. Strengthening of corporate structure

2. Development of competitive products/services. R&D and unification of technology in group companies. (Probably hinting towards a deeper integration of Comerzzia with their acquisitions)

3. Development of commercial capacity

4. Improvement of the effectiveness and efficiency of key operational and support processes.

5. Attract and retain talent

M&A

They tend to let the owner keep a stake to continue to drive the business and product success

Rational behind the M&A is:

Cross Selling

Expanding the offering

Nextt (FY23)

A software solution focused on the catering / restaurant / hotel sector, with POS systems

Part of the reasoning of this acquisition was, in my opinion, to offer retail chains, a solution for their Coffee shops, bakeries…

Not included in FY23 consolidated numbers.

FY23 total revenue: c. 1,7M and EBITDA of 0

CPI Retail and Compudata SA

Both offer services, which were complementary to the already existing solutions at Comerzzia

CPI retail is located in Portugal and might help them with their expansion into Brazil due to the common language

Customers

Customers are mainly large retail chains or industrial companies

Clients generally generate +500MEUR revenues upwards

They also have some very large international retail chains as clients

In the IT-Infrastructure segment they also have some public sector clients

c.1000 clients, in 20 countries, throughout Europe, North America, Latam, UAE and Asia

Sector exposure:

Country exposure:

No precise information is provided, but I assume that the large majority of revenues are currently generated in Spain

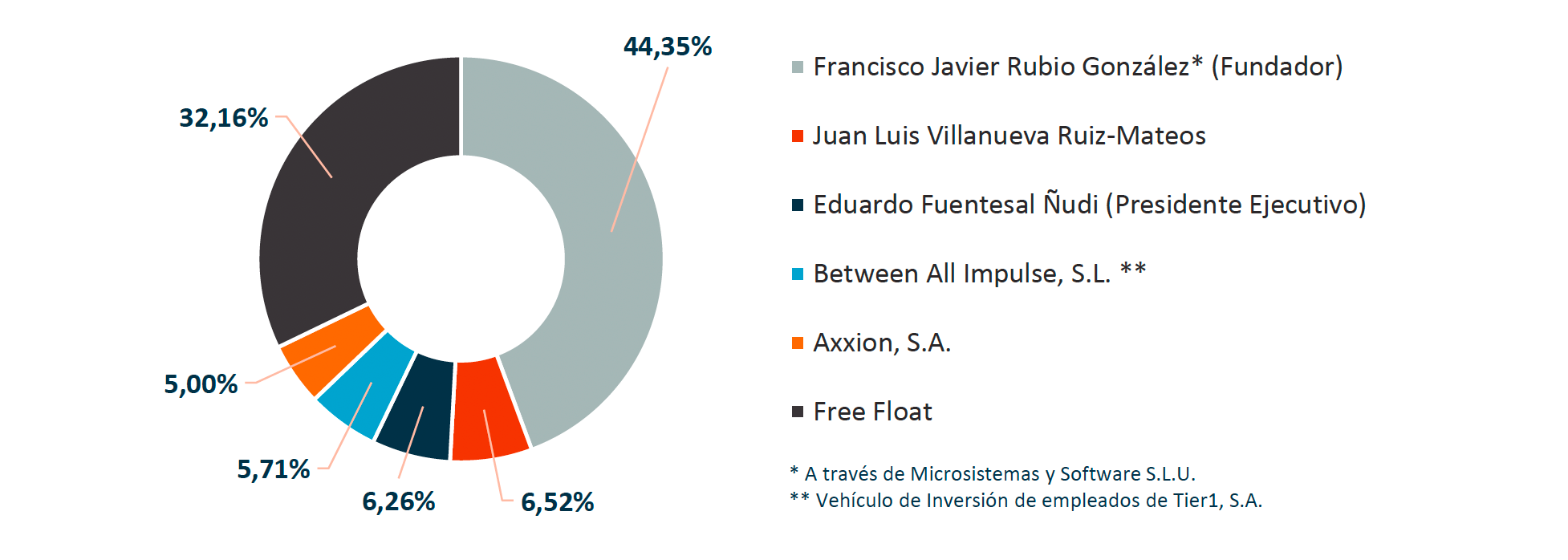

Management and Shareholders

(as of early-FY24)

Franscisco Javier Rubio Gonzalez

Founder, largest shareholder and director of strategy

Eduardo Fuentesal nudi

Corporate Director / President

Since 2012 at the company (till FY21 head of organization and expansion)

Leandro Gayango

COO of Tier1 (It-Services & Comerzzia)

Part of the Management team since 2010

New Independent Board Member: (24.1.2024) - Antonio Somé Carrillo

CEO of Persan

Persan: a 650MEUR revenue Industrial company focused on special plastic bottles for special- and home-care…

In line with their vision to expand their industrial offering

Juan Luis Villanueva Ruíz-Mateos - ex-board

Board Member from FY11-FY23

Might be interesting to see what he does with his shares, after leaving the independent board

Financials

Order Intake:

They only include implementation revenues and one year of licensing fees, as order intake (so extremely conservative).

The IT-Services order intake includes a 2M procurement order, with extremely low margins. And the rest of the growth stems from LT maintenance contracts and development operations

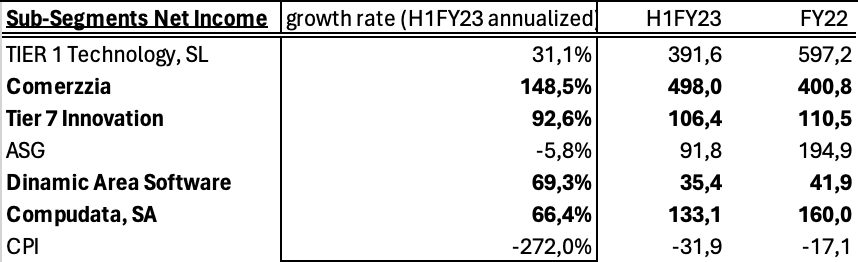

Extreme profit growth of Software Sub-Segments

Quick overview of revenue sources of the companies within Tier1:

Tier7 Innovation and dynamic area = software development

Tier1 Technology S.L. = Software license & IT-Services

ASG, CPI, Nextt, Comerzzia, Compudata = Mainly Software license

This is again shows how strong the operating leverage at Comerzzia really is

(Data from the H1FY23 & This is non-consolidated net income)

Organic vs Inorganic revenue growth

Capex & WC

Capex

Investments seem quite stable overtime

I don’t believe an increase is probable, as a % of revenues

We might even see a decrease due to less investments into Comerzzia

Operating Working Capital:

I define it here as:

-(Accruals, advance payments by customers, Trade payables)

+(Stock, Trade receivables)

16% seems quite normal for a business in this sector, I would expect everything to stay more or less stable going forward as a % of revenues

Maybe even coming down a bit due to less revenues from public sector clients, which usually command better WC treatment

Minority Interests

Comerzzia: 90% owned by Tier1 Technologies S.A. (the holding company)

CompuData: 62% owned by Comerzzia

CPI retail: 51% owned by Comerzzia

Nextt: 52% owned by Comerzzia

ASG: c.81% owned by Comerzzia (acquired in 2017, pre-IPO)

Dynamic area: 55% owned by Tier1 Technologies S.A.

I will touch on the future effects of Minority interests in my Valuation, but in the past and currently it had/has minimal effects (c.4% of Net Income)

Capitalized software spending

Around 2-3% of revenues in the past years, this is something to look out for.

It would be quite easy for them to artificially increase EBITDA by increasing this number

Debt

They have c.1,2M in debt, c.0,7M of it is “soft debt” with 0% interest

Soft debt: From government entities and mostly long-term

Nearly 0 leasing debt

Some insights from a friend who had a talk with the head of M&A at Tier1

He summarized the talk as follows: Essentially, everything I learned was positive, but I never felt like she was talking nonsense. I completely led the conversation and posed my questions, and she answered every question. We only missed one or two due to time constraints.

On SecureInvoice: There may be greater potential with SecurInvoice. This is an e-invoicing solution, and in the future, every company in Spain must send all invoices to the tax authorities.

Regarding their focus: Investors often write to us about ways to increase the stock price, but we want to run a successful business here and make it big on our own strength.

Additional Interesting Facts

Seidor

Large IT-Services consultancy (c.900M EUR Revenue)

They own c.10% of Comerzzia

Have a 50/50 owned Comerzzia - JV for the Brazilian Market

Why IPO

Image & credibility

Capital

Potentially using shares for M&A

General

Share count flat at c.10M since IPO

Press release Okt-FY23: "The Group is currently working on the 2024-2026 Strategic Plan, which it will make public once it is approved by its Board of Directors."

The strategic plan will include:

Reengagement on industrial sector for which they currently already have high value solution

International expansion

Consolidation of Retail leadership

My Thoughts and a quick Valuation

My Assumptions:

IT-Services: (Basically no impact on the overall thesis)

Revenue growth until FY26e:

10% seems reasonable, especially considering the large amount of Comerzzia implementations done

EBITDA-Margins in FY26e:

3%, due to more maintenance contracts and far less trade revenues

I want to be quite conservative for the IT-services part of the business due to not being core part of the thesis, but it wouldn’t surprise me if this segment manages to achieve +5% Margins in FY26e, especially if the implementations of long term maintenance contracts works out

Software

Revenue growth until FY26e:

15% seems fairly reasonable, assuming decent performance from Comerzzia and some optionality in the other Software

EBITDA-Margins in FY26e:

40%, might be a bit too low

I might be under weighting the fixed cost structure of Comerzzia

In the long term margins of c.35-50% seem highly probable

The company only published total revenue and EBITDA figures, as well as revenues by segment for H2FY23, so for H2FY23 I had to estimate segment Margins. My estimates: 0% Margins for IT-Services and therefore 33% for Software.

All of these assumptions only include organic growth figures.

I do believe a fair EV/EBITDA in FY26e would be c.15x, but due to the size, I think a discount will be applied. Therefore, 10x seems reasonable.

In my EBITDA figure I am including the minority interest, which I think is quite irrelevant for the overall thesis. (c.4% of Software EBITDA in FY23.) But It seems fair to assume, to be around 10% of Software EBITDA in FY27, due to the larger relevance of Comerzzia.

Dividend policy:

50% of net Income

FY23e estimated net income 1,5-2M

Dividend Yield c. 3-4%

Concluding thoughts

I haven’t ever come across such an asymmetric situation. On the one hand, I don’t see a lot of downside due to the valuation, aligned interests with management, a large degree of recurring revenues and strong underlying sector tailwinds. On the other hand, I do see huge upside if everything goes right and still a very good upside if some things go as planned.

I think you must have misunderstood something. Comerzzia, the retail solution, is a omnichannel solution, which means it focuses on an array of different offerings.

"Included solutions: scan and go, ERP system, inventory management, e-commerce (great to have an e-commerce and Inventory management in one solution) and many more"

Regarding the international expansion, this might be a good point.

A thing to note though is that the competition everywhere is quite high and in my view its all about finding Sales partners / channels, doesn't really matter where you find them.

And its not like costs would increase drastically due to the international expansion, the Brazil and USA operations are still very small and the expansion via Retex won't require any Capex...

Thank you for a good write up, very interesting company! Wouldn't it be better in the long term if they optimized for growth of the Comerzzia POS? Cancel the dividend and run for a 0% EBITDA for a few years to gain scale? Or is it not as good a product as they say.