Spyrosoft: fast growing compounder trading at a PE of 〜19

Spyrosoft: fast growing compounder trading at a PE of 〜19

A cheap, fast growing polish IT-Services company with short-term headwinds and long-term tailwinds

Disclaimer: This article is for informational and educational purposes only. Do not interpret anything below as financial advice. Always do your research & speak to a financial professional before making investment decisions. See the full disclaimer at the bottom of this article. Stock prices and market value have changed since the time of writing. This is NOT a buy or sell recommendation.

Notes:

-SPR = Spyrosoft

-KW = Konrad Weiske (CEO & founder of SPR)

-upper Management = Management of SPR group

-lower Management = Management of SPR subsidiaries

-eP = external Programmers

-If there is a * next to a heading, there is additional info on this topic in the following PDF.

Biases

A large chunk of my portfolio is invested in SPR, and I've spent many weeks on this write up.

So my opinion might be heavily biased. I tried my best to evade / prevent miss judgements caused by biases but can’t guarantee for anything.

Summary:

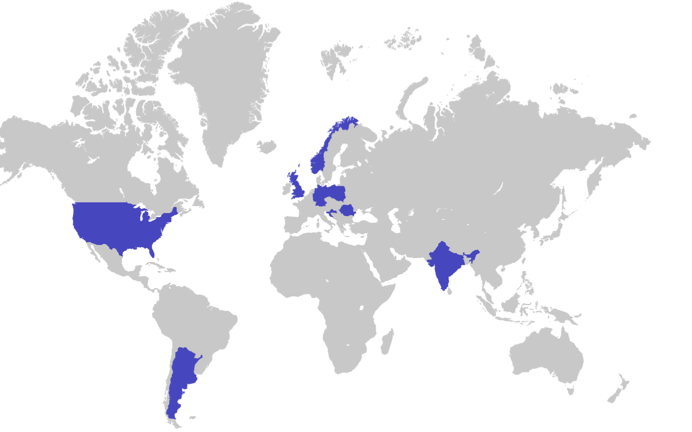

- IT-Services provider, operating globally

- excellent management and incentive structures (in lower & upper management)

- strong long term sector tailwinds, mainly due to an increased need of digitalisation

- short term sector headwinds, mainly due to less demand in some key markets

- decent valuation: PE of around 19

- with a future potential revenue CAGR of 22% & past ROIC of around 40%

KPI Section:

-G&A as % of revenues

-Number of employees

-Cost of goods sold as % of revenues

-EBITDA & EBIT margins

Table of Contents

Introduction

Spyrosoft is a IT-services company with 17 Subsidiaries, in locations all around the world. They were founded in 2016 by KW and 3 others. Through management’s experience and network, the company has managed to capture a large clientele relatively fast, grow their market share and establish a reliable reputation in their targeted segments. They did all this with no help from outsiders and started only with 200k Pounds. SPR IPOed in 2020 in the New connect segment of the GPW.

Business Modell

The Backoffice functions are centralized in Poland or other cheap labor countries to take advantage of cost efficiencies, while the consulting teams and front-office operations are established in local offices for effective client interaction.

Locations

Most employees are in Poland (around 60-80%), followed by the UK, Germany, and the US. The Croatian, Romanian, Norwegian, Indian and Argentinian locations are all still very new & small (sub 50 employees), but all plan to grow very rapidly to a size of around 200 employees each in the next 2-3 years.

Product offering *

Most of their services involve consulting and software programming, with a focus on highly specialized offerings. They are constantly growing their offerings, this year alone they added CRM and Media services.

Customers / Revenue Distribution

SPR mainly targets the mid-market segment since this segment appears to be underserved of quality solutions by smaller companies and is not attractive enough for the larger players in the industry. (SPR also caters to some big clients, for example in the Automotive space...)

Contracts have a duration of 3-6 Months, which in most cases get renewed every time and therefore acts like a long-term contract (most of the projects are long-term).

Most of their customers are located in the UK or the DACH region. The strongest growing region in the future will probably be the US. A while back Jacques Lague joined the Board, with the intent to help SPR expand further into the US, he has 30 years of experience in the US-IT sector.

Share of top 10 clients: around 50%

Biggest client has 12% revenue share.

Due to the very diversified Revenue, the currency risk is fairly well hedged. Additionally, due to the Sectoral diversification SPR is less susceptible to demand fluctuations.

Sector

Trends

Growth:

-Strong growth globally (high single digit growth expected), fuelled by an ever-increasing demand for new personalized software, digitalization, automation...

Employees:

-Most important part of every IT-service company are the highly skilled employees

Costs:

-Inflation and high labor demand are leading to higher labor costs in the long term

Demand

Short-term

-Demand for IT-labor is currently decreasing globally due to a huge wave of layoffs in the ITK sector and an overall cooling down of the economy.

-Demand for IT-Services are currently decreasing

Management's Demand-growth guide 2023: (published on 27.4.2023)

-Automotive sector: Stable rate of growth

-Geospatial: Stable rate of growth

-Industry 4.0 / digital Transformation: Stable (Note: probably mid-single digit)

-Media: slightly negative (mainly due to decreasing Ad-revenues)

-Financials: less growth (Note: probably negative)

-Healthcare: stable rate of growth

-Employee Experience & Education: stable rate of growth

Overall, SPR doesn't appear to be heavily impacted by the short-term decrease in IT-service demand. While the revenue growth may decelerate significantly compared to previous years, it may not be a major concern considering the high growth rates experienced in the past.

One potential issue is that SPR hired a large number of new employees last year (600) and may need to bench more of them than in prior years (low single digits instead of around 1% of the labor force), which will affect margins. However, the decreased costs for external programmers, and lower wage growth for normal employees, could potentially offset this impact.

In Q1 2023, the G&A costs increased by 20% and the gross margins improved by 1,3% points. This indicates stable pricing power and decreasing costs for external Programmers (gross margins), but an increase in benched Employees (G&A).

Long-Term

Labor:

KW constantly stresses, that the demand for specialists exceeds the available supply.

While the current economic downturn may temporarily alter this situation, the ongoing pressure for increased digitalization suggests that the demand for specialists will continue to rise steadily, leading to higher wages.

Services:

KW stresses that in the long term, there will be a higher demand than supply for IT services. However, acquiring clients remains challenging due to trust issues and the high costs involved. Moreover, the primary driver of IT demand is not gaining a competitive edge, but rather the necessity to stay relevant. This viewpoint is corroborated by multiple studies.

Employees

Employees are the backbone of IT-service companies, and SPR recognizes the importance of attracting and retaining talent. This focus is consistently highlighted by the management in press releases and interviews. Their goal is to reach 3,000 employees by early 2026, a significant increase from the current 1,410.

Currently, 50% of their employees have more than four years of experience in the sector they serve, while 25% have more than two years of experience.

In employee surveys, SPR received positive ratings in key areas

Good working atmosphere – 84%

Employment stability – 80%

Good teams – 81%

Global expansion strategy

SPR is entering new markets such as Argentina, India, and select Eastern European countries.

(And also plans to expand into the middle east in the future). SPR intends to have a large double-digit percentage of employees from these new markets, in the long term probably around 30-50%.

This expansion aims to access a larger pool of highly skilled and cost-effective employees, with potential cost savings of up to 50%. These wage costs are already 20-40% cheaper than the IT-labor in markets they serve. Further benefits of the expansion are global labor diversification and having the ability to serve clients in various time zones.

Bench

As previously highlighted, one area of concern is the number of employees without project assignments. Currently the figure is around 1% and will probably accelerate into low single digits. Managing this will be crucial for future Profit margins.

Stock options Plan for IT-Specialists

As part of the strategy 2022-2026 (which I will dive into in a later chapter), SPR plans to grant approximately 5% of shares as stock options to key employees. This allocation is specifically targeted towards IT specialists and senior employees, rather than the upper management. The objective behind this initiative is to incentivize and motivate employees to actively contribute to the implementation of the new strategy. By offering stock options, SPR aims to foster a stronger connection between the employees and the SPR Group, aligning their interests with the long-term success of the company.

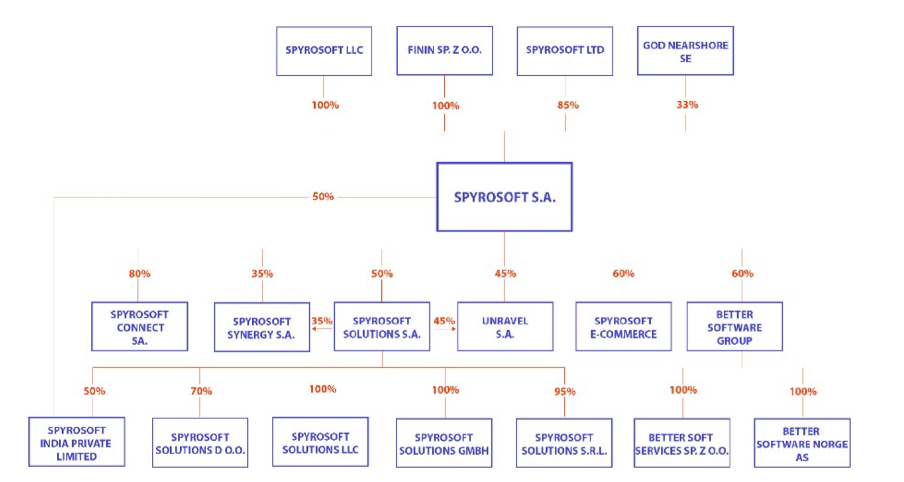

Company Structure & M&A and Ventures

Company Structure

SPR is composed of 17 subsidiaries, some of which were acquired while others were internally founded. Each subsidiary operates with a high level of decentralization, taking full responsibility for its own sales generation and recruitment activities. The branches specialize in specific geographic or product areas but maintain constant collaboration and knowledge exchange as different business divisions. Cross-selling plays a significant role in their operations, and in the past 48 months, SPR has acquired or founded approximately 10 subsidiaries.

Incubator Strategy

SPR follows an incubator strategy by seeking out experienced IT professionals interested in starting a company in an untapped geography or product category. These IT professionals often hold senior managerial positions in prominent IT firms, prior to working for/with SPR.

In exchange for establishing their companies under SPR, founders are offered equity ranging from 10-40% of the total ownership. Additionally, a relatively small amount of cash, typically ranging from 10,000 to 100,000 euros, may be provided as part of the agreement.

"we establish new companies under the Group with people who have expertise in a specific industry or technology, who want to run their own business, and who can reach both potential clients and experienced employees" - Konrad Weiske (7.4.2023)

Benefits for the founders:

-SPRs expertise

-cross selling

-financing

-equity

-independence

Benefits for SPR:

-highly incentivized entrepreneurs with a lot of very specific sector knowledge working to maximize subsidiary growth and profits

-access to a broader base of Acquisition opportunities, experienced employees and Customers (founders sometimes bring whole teams form other bigger, better capitalized companies to the subsidiaries)

Acquisition strategy

Similar to the incubator strategy but focuses on companies that already generate revenue and have established structures. Trust and longstanding relationships between upper management are crucial prior to the acquisitions. Trust is vital within the decentralized structure.

Acquisitions by SPR are typically inexpensive, with the company paying a single-digit multiple of the target company's net income. This favorable pricing is attributed to similar reasons that attract founders to join SPR, such as leveraging SPR's expertise, cross-selling opportunities, independence, and the offer of equity.

Acquisition goals:

-enlarge product portfolio

-geographic expansion

-access to Employees

-access to technology & expertise

Recently Acquired / Founded Companies

2021

-Spyrosoft Solutions doo, 35% stake for 15kPLN

-Spyrosoft Solutions GMBH, 50% stake for 110kPLN

-Spyrosoft Synergy S.A., 60,5% stake for 70kPLN

2022 and Q12023

-Spyrosoft Ecommerce S.A., 60% stake for 60kPLN

-Spyrosoft Solutions S.R.L (Romania), 47,5% stake for 88kPLN

-Better Software Group S.A. Capital Group (Norway + PL), 60% stake for 20mPLN

-Spyrosoft Connect S.A., 80% stake for 0PLN

Ownership & Management & Culture*

(An overview of all management teams, with some information on their past work experience is provided in the extra document)

Quality of Management

Two notable aspects stand out in the companies Management:

1. The large majority of people in lower and upper management positions have extensive experience in management and, more importantly, in IT positions. This first-hand knowledge enables them to have a deep understanding of the requirements for efficient IT labor.

2. A large majority of the upper and lower management team possesses over 15 years of industry experience. Notable examples include KW (CEO) with 20 years of experience, Sebastian Łękawa (co-founder) with 20 years, Wojciech Bodnarus with 18 years, the CEO of SPR-Solutions with 17 years, and the entire BSG team, which has been active in IT since the late 1990s. This wealth of experience brings a strong foundation of industry knowledge and expertise to the company.

Culture

The culture at SPR is employee-focused, highly decentralized, and emphasizes a high level of independence and self-responsibility. The management's primary goal is to create the best possible environment for employees, making their work easier and more effective so they can focus on the essential task of creating software for clients.

CEO KW consistently stresses the bottom-up approach, where the management's role is to facilitate and support software engineers in their work. Furthermore he stresses, that any employee at any time can talk with him about ways of improving things.

SPR might just have a great IR/HR team, but in the countless interviews available on the website, SPR management come across as genuine, open, focused on learning, and trusting in their colleagues & employees. Consistent with what KW talks about.

In another interview, KW highlighted that his primary responsibility as CEO is to manage the various Managers of the subsidiaries, ensuring clarity and alignment of future goals and direction. This approach is essential, as it provides a central coordinator with a vision for future culture, growth, and other important aspects in a decentralized system like SPRs.

Owner oriented Management

Three Key themes:

(1) Upper Management takes very low compensation, (2) owns a large number of shares and (3) lower Management teams often own large stake in their respective Subsidiary.

(1) Yearly Compensation

Konrad Weiske (CEO) = 60kPLN

Wojciech Bodnarus (CFO) = 60kPLN

Slawomir Podolski (COO) = 60kPLN

Sebastian Lekawa (Board Member) = 27kPLN

Total management compensation = 207KPLN (= 45k Euros or 48k USD), its lower than most employees’ salaries.

(2) Shareholder structure (as of May 27 2023)

(3) Ownership of lower (subsidiary level) Management:

In most of its subsidiaries, SPR holds ownership ranging from 30% to 85%, while the remaining 70% to 15% is owned by the management (and founders) of each subsidiary. Despite this, more than 70% of the earnings still belong to SPR, primarily due to its significant stakes in the most profitable branches.

Notably, there is no involvement from private equity firms or external entities in the ownership structure.

Looking ahead, Spyrosoft plans to buy out the lower management of its subsidiaries, offering stock or cash, at a fixed EBITDA multiple in 2026 or 2027. This buyout strategy creates a strong incentive for lower management to maximize results until then, aligning their interests with the shareholders in the medium-term.

Intive or SMT Software

(where it all began)

In general, it is noteworthy that a significant number of lower management teams within SPR have a history of long-term professional collaboration before joining the company (usually in the realm of 5-10 years).

Furthermore, it is crucial to highlight that a significant number of co-founders, upper management, and some initial lower management team members had worked together at SMT software (later Intive) for 5 to 20 years before they joined/founded SPR. The most recent addition from Intive joined SPR in 2019. Therefore, I think it is indeed relevant to briefly have a look at SMT/Intive.

SMT Software, founded in 1999, had its main offices in Germany, Poland, and the Netherlands and experienced significant revenue growth over the years (over 30% for many years). In 2016, SMT Software merged with two other IT-service companies to form Intive. In the same year, a private equity fund acquired 90%.

The newly formed entity, Initve, had a similar, but smaller product range to SPR, it reported a revenue of €60 million and had 1,200 employees in 2016 (of which 2/3 were from SMT). Over time, Intive expanded its workforce to 1,600 employees in 2018 and reaching 3,000 employees by 2023, with an estimated revenue of around €450 million and an NPS score of 75. The employee distribution is estimated to be approximately 10% in Germany, 20% in Poland, and 20% in Argentina. Most of Intive's revenue, around 50%, is generated in the USA.

Following the merger, KW left the comapny and founded SPR, others from Intive joined him in 2016 or would join within the next three years, due to being dissatisfied with how the private equity firm managed things and the belief that they could handle the situation more effectively.

KW, a former board member of SMT Software, and Sebastian Lekawa, the founder, had worked together with other members of SPR's current upper management for a period of 5-20 years, at SMT/Intive. They gained valuable experience from the time at SMT/Intive, which involved rapid global expansion and successful market penetration in regions such as Argentina and the USA. This holds great relevance to the current situation of SPR and its goals to further expand globally but is especially relevant for the expansion into Argentina and the US.

Poland

Poland has several advantages that make it an attractive destination for international IT services companies:

1. Highly Qualified IT Personnel: a large and continuously growing pool of highly qualified IT Labor. (around 15,000 IT graduates annually)

2. Cost Advantage: Labor costs in Poland are relatively lower compared to many other countries where IT services are provided.

3. Central Location in the EU: makes it easily accessible to clients across the region.

4. EU Membership: benefits from a stable political and regulatory environment. And offers easy access to a broad market.

5. High Rate of English Speakers: particularly in the younger generation.

6. Strong Economic Growth: long-term high single-digit GDP growth, indicating a robust and expanding economy.

7. Low Cost of Living: Poland has a relatively low cost of living compared to client countries.

8. Stable Political Environment

9. Business-Friendly Environment: The Polish government has implemented various initiatives and incentives to foster a business-friendly environment.

For a more detailed analysis of the Polish economy and its potential as an investment destination I can warmly recommend the "Polish Equities" paper by Jenga.IP. It offers in-depth insights and case studies on the Polish market, it also highlights some risks, like the inflation situation.

Moat / Competitive Advantages

Barriers to entry

The whole IT-services industry doesn't have any classical Moats, there isn't any kind of substantial IP or expensive assets which would lead to barriers to entry.

The only real barrier to growth is the number of employees you can recruit, which is highly correlated with compensation, so if you’re willing to burn loads of cash you can scale quick.

“In the IT industry, we all need to constantly acquire new competencies because when you look at the direction in which the IT industry is developing, you can see that simpler things can be automated. ... So our goal is to have as many people as possible in the company at the technical lead, principal, or senior level." - Konrad Weiske (7.4.2023)

Competitive Advantage

Switching costs, once you work with some firm and trust them you don’t really want to switch as long as services are good, and prices stay competitive.

Client trust, SPR gained client trust through expertise, its unique culture, and recommendations, with 83% of services sold coming from client referrals.

Product Portfolio, SPR can adhere to very differentiated and growing needs of a customer, due to the highly diverse product portfolio, other companies often have all their competencies in one field. (Very relevant for competitions for large contracts)

Employees, there is a limited pool of very high-quality IT professionals and a very large demand for these, so its highly important for any company wanting to stay competitive to continue to attract and keep these professionals. SPRs global presence gives them a broader base of potential employees.

Management

SPR's experienced (lower & upper) management teams with an owner mentality create an competitive advantage by being highly agile, decentralised and emphasizing long-term value creation (incentives are aligned to create the maximum lng term value for shareholders).

A lot of IT-Services companies upper management is full of people who never (or only for a short time) have worked as programmers or similar roles in IT which obviously is a huge advantage for SPR. (Due to the abundance of experienced Management)

"Spyrosoft was founded by people who worked in IT, primarily in technical positions. This perspective has helped a lot. I know what I would expect from the company as a developer because I used to be one not so long ago." - Konrad Weiske (7.4.2023)

Furthermore, SPR's CEO can dedicate his full attention to strategic initiatives, M&A, and managing subsidiary level Management teams, without being distracted by operational matters. Also, SPR's ability to offer equity to new lower management teams enables them to attract highly skilled and experienced professionals from top firms, ensuring strong lower management teams going forward.

Culture

A strong culture centred around IT professionals fosters employee retention, while the LTIP (long-term-incentive-program) aligns top employees with company goals.

Additionally, the openness of management and flat hierarchy leads to a stronger discourse between management and Employees which again leads to better outcomes for everyone including better retention.

Structure

SPR's decentralized structure promotes agility, resilience, and the possibility for fast growth in various areas simultaneously. (Also partially due to the low need of CapEx spending)

Low-cost labor

Low labor costs compared to IT service providers in DACH, US, and UK give SPR a competitive edge, due to offering same or better-quality products at a lower price.

All of this leads to efficiency growth, better services/products, happier employees & customers and therefore to more trust from employee and customer side, which is Key.

Something to look out for in the future, as signs of efficiency growth:

Rev/Employees

EBIT/Employee

external Programmer costs / Rev

Employee Wage costs / Rev

Spyrosoft Strategy 2022-2026

-Published in Q1FY22

-A comprehensive plan for the finical years 2022 till 2026 (FY26 = ending early 2027)

Goals for FY2026

Revenue CAGR: growth rate of 25-35% annually (Given the high growth rates in 2022, SPR "only" needs to grow 13-24% per year to reach the FY2026 goals)

EBITDA Margin: 11-14% (FY22 = 16%, Q1FY23 = 12,2%, lower long-term estimates due mainly to higher expected Labor costs)

Workforce: minimum of 3000 associates.

Key ingredients of the strategy

Organic growth: Focus on cross-selling to existing customers and acquiring new customers.

Expansion of portfolio: New specialized companies through acquisitions and organic growth to complement the existing portfolio of service.

Establishing new R&D center’s: Currently exploring opportunities to open R&D centers in locations beyond Poland, such as Argentina, Romania, Middle East, and India. (R&D centers = new office for programmers)

Increased marketing efforts: Particularly targeting markets in the USA, UK, DACH and Nordic regions to enhance brand visibility and attract new clients. (No signs of this a year later, marketing spending = 0)

Inorganic growth: Strategic acquisitions to accelerate growth.

Consolidation of shares within Spyrosoft

-Planned for 2027

-Based on EBITDA*Market multiples

-Achieving 100% ownership of all subsidiaries

-Incentives for current subsidiary shareholders to maximize EBITDA growth

International IPO

-Planned IPO on a major EU or USA exchange after consolidation

-Potential dilution in 2027 for the buyouts, with no impact if stock is not undervalued at the point of dilution

Share options Program:

Around 5% of shares in total, from 2022-2026

With the goal of encouraging employees to implement the new strategy and fostering a bond between SPR and its key employees. Around 600 employees are getting share via this program.

P&L, Balance sheet and Cash Flows *

-I will provide a quick overview of some important numbers, the full P&L and some Balance sheet + Cashflow + Employee/Labor-cost + extensive Valuation calculations are in the attached Excel file.

Overview (Pre Q1FY23 Numbers):

Revenue

growth: 10x since 2018

Margins:

-stable since 2 years, before that some fluctuation (always strongly positive)

Gross-Margin = 33%

EBITDA-Margin = 16%

EBIT-Margin = 13%

Net Income-Margin = 11%

In 2020, SPR achieved its highest EBIT and gross margins, reaching 18% and 37% respectively. This was primarily driven by a decrease in costs, particularly in spending on external programmers. However, as the company increased its expenditure on external programmers due to the acceleration of growth, the margins subsequently declined.

Costs

labor:

62% of revenue is spent on labor

(Including 41% of revenue for external Programmers = 70% of third-party services costs, note 2 in annual)

licensing

21% of revenue is spent on licensing (mainly Software) (= the other 30% of third-party services costs)

D&A & CapEx

2,6% of revenue is spent on D&A

2% of revenue is spent on CapEx (very stable over time)

G&A

19,3% of revenue is spent on G&A and decreasing over time (prior to Q1FY23), due to a very slim HQ and advantages of scale

Profit attributed to Minority shareholders:

Used to be around 22% of earnings (PrFY22) and is now 30%, due to partial BSG Acquisition (but full consolidation), and them being so highly profitable.

(in Q1 its at 24,5%, due to the bad BSG results)

Cashflow

NWC

+33m Receivables from BSG in 2022

NWC changes 2022-NWC changes 2021 = 0, (+11m in 2022 and -11m in 2021 (excl. BSG))

FCF / Net Income

80% (excl. NWC from BSG)

operational Cashflow is on average equal to Net Income

Balance sheet:

Pensions

Due to the age structure of employees, no provisions are created for retirement severance pay.

liabilities

9,3m (increasing)

Cash

34m (increasing)

Q1FY23 (published March 2023)

Rev. up QoQ 4%, YoY = 74%

Gross Margins up by 1,3% (absolute)

-driven by decreasing costs for external Programmers & stable pricing power

G&A costs up by 5,5% (absolute)

-due to Increase in Bench

Leading to a EBITDA-margin decrease from 16,2% in FY22 to 12,2% in Q1FY23.

Valuation

I will heavily rely on the goals set in the 2022-2026 Plan for my valuation. (Quick reminder: SPR aims for an EBITDA-margin range of 11-14% and a revenue CAGR of 25-35%, with a target CAGR of 33%)

Revenue:

By factoring in substantial revenue growth in 2022 and keeping the revenue CAGR targets unchanged for 2023-2026, SPR's CEO probably foresees a moderation in growth expectations for the upcoming years in comparison to the previous period.

There is a possibility that my interpretation of the presentation is incorrect, and the Revenue CAGR is intended to represent annual growth goals rather than cumulative growth over the five-year period.

In the Q1 letter to investors, KW indicated that he foresees the revenue growth and EBITDA margins in FY23 to be on the lower end of the guidance provided in the 2022-2026 Plan. This suggests that the Revenue CAGR is intended as a yearly goal.

Regardless of the interpretation, I will consider the goals as cumulative growth targets rather than yearly ones. This provides a margin of safety.

Future Opportunities for revenue growth

1. Expanding service offerings through acquisitions or organic growth

2. International expansion: especially into the United States and further expansion into Europe. The addition of a new board member from the US and the establishment of an office in Argentina and the very strong employee growth at the location are indications of their expansion plans.

3. M&A to leverage the fragmented market and gain access to skilled employees, new services, and a broader customer base.

4. Creating IP: Currently, it is not a significant part of revenues, and the only existing example of IP is in the geospatial business unit. The potential for creating other forms of IP presents an opportunity for the future; however, it is important to note that this is highly speculative and may not materialize at all.

I believe that SPR has a strong potential to achieve the management's goal of a 33% revenue CAGR from 2022-2026. With strong sector tailwinds, highly incentivised management teams and loads of expansion opportunities, the company is well-positioned to realize this target. This would imply a revenue CAGR of 22% going forward.

EBITDA:

In the short run:

-Slowdown in overall demand in the IT services sector

-Unassigned employees (bench), rising => G&A costs up => EBITDA down

-Lower demand for external programmers => EBITDA up

-Lower wage costs for new employees => EBITDA up

Bench costs are expected to exceed eP costs as SPR has a surplus of employees, due to expanding its employee base rapidly in anticipation of further growth, resulting in an excess supply of employees, in current times of lower demand. On the other hand, the demand for eP remains relatively high, indicating that their costs will likely decline at a slower pace.

In the long run:

-Strong long-term demand growth expected

-Fully occupied workforce reduces G&A costs => EBITDA up

-Recovery in demand for external programmers => EBITDA down

-Increased employee demand => higher wages => EBITDA down

Net Income conversion to FCF

-No significant increase in CapEx spending relative to revenue expected

=> Net Income, aligned with FCF excluding NWC

-NWC changes generally very stable (so more or less 0)

In my opinion, an EBITDA margin of 12% in FY2026 appears quite likely and conservative. However, this outcome will be highly dependent on the overall macroeconomic situation. It is important to note that the demand for IT services cannot be postponed indefinitely, and at some point, there will be a recovery in demand even in more challenging macro conditions.

In summary, my base case scenario for SPR:

-Revenue growth of 22% annually

-EBITDA margin goal of 12%

-D&A costs at 3% of revenue (Average since 2018 + 0.5% margin of safety)

-1,5% annual increase in shares outstanding

-27% of net income attributed to minority shareholders

-Tax rate of 20%

Based on these assumptions, the projected EPS for FY26 is 43.

In terms of valuation, I believe a fair PE multiple range is 15-25. This would result in a share price range of 645 (15x) to 860 (20x) to 1075 (25x) in FY26. Considering the current share price of 450, this implies a price CAGR of 11-26%.

Notes:

1. Growth may not be smooth but rather lumpy, influenced by economic conditions.

2. EBITDA margin and revenue CAGR estimates are conservative compared to the past.

3. Assuming a more relaxed macro environment, EBITDA could recover to higher levels.

4. The % net income attributed to minority shareholders could also be a lot lower if BSG doesn’t manage to grow as fast as the rest of the subsidiaries, due to a prolonged Media-Sector slowdown (In Q1 its already down to 24,5%)

Key Risks

Currency risk: As SPR deals with foreign currencies, fluctuations in exchange rates could impact its financial performance. However, the company's geographically diverse revenue streams provide a level of protection.

Wage inflation: The IT sector faces the challenge of wage inflation, and SPR is not immune to this risk. However, the management has experience in managing higher labor costs, and the absolute wage costs per employee remain low compared to international peers. Additionally, by expanding into even cheaper labor markets SPR will be able to counter some of these effects.

M&A and ventures: There is a risk of not finding suitable acquisition targets or compatible entrepreneurs for expansion, which could limit SPR's growth.

Employee retention: Retaining top talent and managing employee turnover is crucial for SPR's success.

New Employees: Growth mainly comes from employing more consultants / engineers. So a failure in attracting new employees is a key risk.

Sector-specific risks: Changes in technology, market trends, or disruptions in the IT services sector could impact SPR's business and competitive position. (e.g. would be AI related services). KW said in a recent interview that he believes that the risk of disruption to SPR's operations is low as long as the company continues to employ a significant number of highly capable programmers.

Client relationships/trust: Establishing and maintaining strong client relationships is vital for SPR. Any loss of key clients or failure to meet client expectations could have negative consequences. This risk is especially relevant, because a large part of new revenues is derived by referrals (83% in FY22).

Revenue concentration: SPR's revenues are concentrated among a few clients and sectors, which poses the risk of revenue loss if key clients switch providers or if sectors experience substantial downturns.

Competition: The IT services sector is highly competitive, but SPR can mitigate some part of this risk by offering high quality and relevant services at competitive prices.

Pricing power: The overall demand for IT services often exceeds the supply of qualified labor, providing providers with some limited pricing power. However, this gap may narrow in the short term and expand again in the future.

Dependency on key people in management: The experience and independence of SPR's upper and lower management mitigates the risk of key personnel loss, such as the CEO. However, post-2026, when SPR buys out all lower management, there could be a potential risk, of a loss in lower management teams. To address this, I assume that some of the lower management's stakes in subsidiaries (if not all) will be converted into SPR stock, ensuring alignment of interests and minimizing any potential disruptions.

Short-term contracts: SPR's reliance on short-term contracts, which can be easily canceled within 3-6 months, introduces a level of uncertainty in revenue stability.

Closing thoughts:

In my opinion Spyrosoft presents a compelling risk/reward situation with its strong management, favorable industry tailwinds, strategies to address challenges and a decent valuation.

But it’s important to keep in mind, that SPRs Q1FY23 results weren’t very good, relative to the past, and there is the possibility for existing headwinds to intensify before reversing again.

Sources

(besides the Annual reports and other “official fillings”)

Interviews with KW:

1. https://spyro-soft.com/blog/spyrosoft-created-by-it-experts-for-it-people-interview-konrad-weiske

2. https://spyro-soft.com/blog/another-great-year-spyrosoft-interview-konrad-weiske

3. Interview on Spotify with the CEO (Highly recommended)

4. Interview with the CEO of the UK Branch on Spotify

5. I can highly recommend the Salary guide from Hays to get a quick overview of the disparity of labor costs in different countries