Covalon Technologies Ltd

A stock returning +290% YTD - poised to perform strongly in the future?

As always,

I am very grateful for any feedback.

Do your own due diligence. Fact-check anything I say. It’s always possible that I made minor or major mistakes, even though I rigorously try to avoid them.

Disclaimer

This article is for informational and educational purposes only. Do not interpret anything below as financial advice. Always do your research & speak to a financial professional before making investment decisions. Stock prices and market value have changed since the time of writing. This is NOT a buy or sell recommendation.

Why am I writing this report now?

I have been owning COV.V since their Q2FY24 numbers (22.May), but decided to not write a Report due to 1. Time constraints 2. The write up by

covering the thesis thoroughly.After pitching the idea to numerous investors, speaking with individuals well-versed in the company and its industry, and conducting thorough independent research, I thought I might provide some value by writing a short pitch.

Covalon Technologies specialises in selling collagen-based dressings (plasters) and antimicrobial vascular access products. These patented, consumable products create highly recurring revenue streams.

Covalon’s current CEO (Brent Ashton), who joined the company in January 2024, has driven a significant turnaround in the company's performance. Before he joined the firm, the company faced severe challenges, but his strategic decisions—shutting down underperforming segments, optimising operating expenses, and prioritising the less volatile, higher quality and higher growth U.S. business—have yielded impressive results.

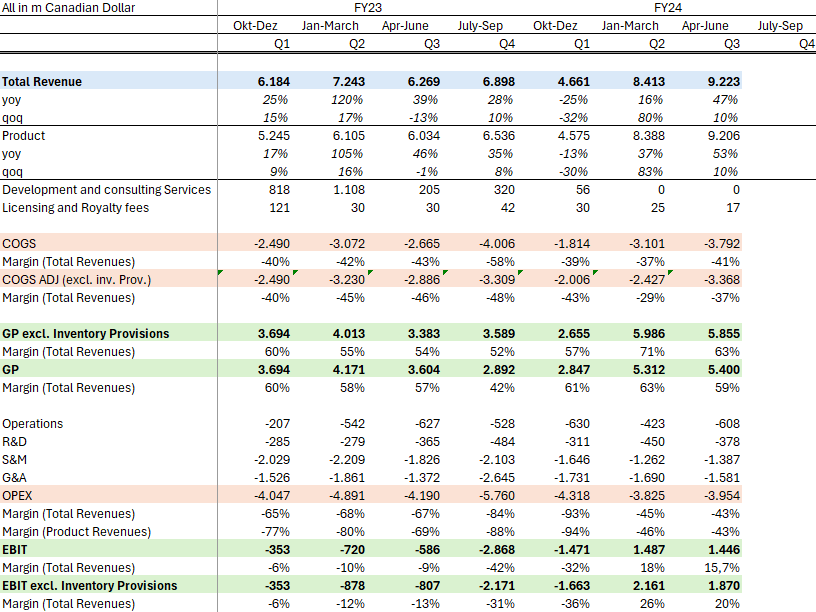

The gross profit margin improved markedly, rising from 52% in Q4 FY23 to 63% in Q3 FY24. Similarly, the EBIT margin shifted from -31% to 21% over the same period. These margins exclude inventory provisions, which appeared due to past managements mistakes.

Covalon holds a strong niche in its collagen-based wound care segment (est. 70% of revenues1), commanding approximately 15% market share, according to the CEO2. The company achieves some differentiation from competitors by delivering high-quality products at a cheaper price. Nevertheless, Covalon’s collagen products are commodity-like.

In contrast, its vascular access segment (est. 30% of revenues) has a market share of less than 1%, but with a significantly larger market size, it presents the main area of growth and attention going forward. In this segment there are strong differentiating factors based on patents and formulation of products. The most important result being, that their product is a lot softer towards the skin, then comparative products.

YTD growth through Q3 FY24 has been impressive in both segments. The vascular access segment grew by 59%, while the collagen wound care segment achieved 62% growth.3

The recent growth in Covalon's collagen segment has likely been driven by two key factors: its new role as the sole distributor of collagen products for a major distributor and the market weakness of a competitor, Solventum, following its spin-off from 3M. This has boosted run-rate revenues, but the growth rates are expected to normalise, likely by Q2 FY25.

In comparison, the vascular access segment’s growth has been fuelled by a strategic shift and targeted investments. The CEO has emphasised a vision for its expansion, driven by the question “how do we double that business (the vascular access segment) in the next two years and then how do we double it again?”4

The CEO confirmed in a private call with me that the collagen and vascular access segments have similar profit margins, suggesting a shift in revenue mix wont hurt the bottom line.

The company is currently (Q3FY24) trading at a run-rate EV/Earnings of c.14 (Price per share 3,9 CAD and 16M Cash). And I estimate EV/E for FY26 to be roughly 10.

has a great write up delving deeper into the business, strategy and some of the core growth drivers in the past quarters. With my shorter report on COV I wanted to point out a few risks and the general thesis in a compressed manner.The Upside

Collagen / Wound Care Segment

Once the LTM revenues and the run-rate revenues are aligned I believe that this segment should grow more or less in line with the collagen market, with market growth projected to be 5-10% p.a.

The segment might also gain some additional market share, but due to the very consolidated nature of this market large growth shouldn’t be expected

Vascular Access Segment

Market share expansion, through cross selling to existing clients and by gaining new ones will be the core driver of growth, according to the CEO

With a goal of doubling the revenues every 2 years

The CEO also has stated in a private call with me in August, that he aspires to double the total revenues in the next 3 years and that the medium-term EBIT margins target is 20% for the overall company.

The Downside

Collagen Segment Risks

Covalon as a temporary solution to the Solventum problem

Solventum, holding 40–80% of the collagen market share5, has been weakened by logistical and input cost disruptions following its spin-off from 3M. According to the CEO a substantial part of YTD growth was driven by this dynamic.6

Should Solventum stabilize its operations, these customers may revert to their previous supplier.

Counterpoints to Mitigate Concern:

Collagen represents a small subsegment of Solventum’s overall business. Given its limited market size relative to other areas, Solventum may choose not to aggressively compete in this segment, leaving room for Covalon to maintain share.

Solventum previously benefitted from 3M’s cost advantages. Post-spin-off, higher input costs may present a structural disadvantage, keeping its pricing less competitive.

Since COVID-19, hospitals have increasingly prioritized supplier diversification to mitigate supply chain risks. Solventum's weaknesses acted as a door opener, enabling Covalon to establish relationships with new customers. These newly, secured footholds could prove durable, as hospitals may now view Covalon as a alternative supplier, even in the case of a Solventum recovery.

Covalon's shift of focus to the U.S. collagen market earlier this year, coupled with improved sales and distribution management, has likely been a part of the growth function, independent of competitor weaknesses.

Dependency on Key Distributors

This segment relies on a handful of distributors to drive sales. The departure of any one distributor could significantly disrupt revenue streams.

Competitive Pricing Pressure

Solventum is positioned as the highest quality but also the most expensive solution.

Following their price increases due to a worsened cost structure post-spin-off from 3M, many hospitals began transitioning to Covalon. Although Covalon's offerings are slightly lower in quality, they provide a significantly more competitive price, particularly after Solventum's price hikes.

If this situation normalises or if Solventum reduces prices, Covalon could face a significant threat.

Low-Cost Competition from China

According to the CEO, low-quality, cheaper competitors from China could enter the market and exert downward price pressure, potentially forcing COV to reduce collagen product prices by up to 10% in the medium term7.

Cyclicality of Collagen Wound Care Studies

Trends in collagen wound care are partially driven by the publication of positive and negative studies. A secondary market distributor that I talked to noted alternating cycles of hype and downturn, in the Collagen Wound Care market depending on these studies.

The last notable positive study was in late FY23.

While unverified and for me personally very hard to confirm or deny, this cyclicality could impact demand.

Vascular Access Segment Risks

Ineffective OPEX Investments

Significant investments in sales and operational staff have been made to accelerate growth in this segment. If revenues do not scale as expected, margins could deteriorate.

CEO-Specific Risks

Capital Allocation Concerns

The CEO's track record as a capital allocator remains unproven, raising concerns about the potential prioritisation of empire-building over sustainable, profitable growth. His frequent discussions about M&A suggest that an acquisition within the next five years is likely, this comes with the inherent risk of overpaying for targets.

The CEO has extensive experience as a former VP of 3M's Medical Solutions unit, which directly competes with Covalon in both collagen and vascular access. His operational expertise is evident in the company’s turnaround but may not translate directly into effective long-term capital allocation.

Closing Thoughts

I like the CEO, his professional track record speaks for himself and the successful COV turnaround is another indicator of competence. Additionally the Business Model seems to have some very favorable characteristic and I believe the risk reward for this Stock is favorable. But due to being invested quite early and the discussed tail risks, I am probably going to trim some of my COV position, which currently is about 12% of my portfolio. But I plan to stay a long term shareholder for many years, as long as the CEO continues to deliver in the Vascular Access segment.

Financials

NO GUARANTEE FOR CORRECTNESS

Note: Taxes & Financial costs are roughly 0, and I assume they wont have to pay any taxes until FY28/FY29, due to past losses.

Estimated by me, based on CEO commentary

September 2024 MCC presentation

September 2024 MCC presentation

September 2024 MCC presentation

According to the CEO

September 2024 MCC presentation

August 2024 Call with the CEO & Me

$COV.V $CVALF Covalon and Tariffs

After getting a question on tariffs under my last twitter post, I delved deeper into the topic and also wrote to the CEO about it. In this Thread I will share some interesting insights:

In a very unlikely scenario where Trump raises tariffs to 25% on all goods from Canada, what would be the response and effect on COV?

COV only manufactures collagen products in Canada and to a small extent in the US. More than 100% of demand can be produced in either facility.

"So while we would of course prefer not to see a sustained 25% tariff on products manufactured in Canada or Mexico, we have a number of options to partially or potentially completely mitigate the financial impact of a sustained 25% tariff. All options are on the table" - CEO

Competition:

"To the best of my knowledge (they have to print country of origin on the packaging), the two biggest players in the space (Solventum and Medline) manufacture in Europe. I also know that the majority of low cost brands sold in the US are made in China." - CEO

Conclusion:

All in all, the tariff risk seems to be more of an opportunity than an actual risk, given the ability to mitigate it and the fact that low-cost players would need to either increase prices or lower margins in the event of tariffs. Additionally, other companies like Solventum and Medline wouldn’t be as flexible as COV in handling possible future tariffs on goods from Europe.